What is a Shareholder Loan? A Comprehensive Guide for Business Owners

Introduction

In this comprehensive guide, we’ll dive deep into the world of shareholder loans, exploring their purpose, advantages, disadvantages, tax implications, and repayment considerations and how financial experts can guide you through them.

Understanding Shareholder Loans

Definition and Purpose

Structuring Shareholder Loans

1. Term Loans: These loans have a predetermined repayment schedule, outlining the specific amounts and dates for repayment.

2. Credit Lines: Shareholders can access funds from the company whenever necessary, similar to a revolving line of credit.

It’s important to note that if the loan is not repaid within a specified timeframe, it may be considered a distribution to the shareholder, potentially leading to tax consequences.

Let’s look at the advantages of taking shareholder loans from customers.

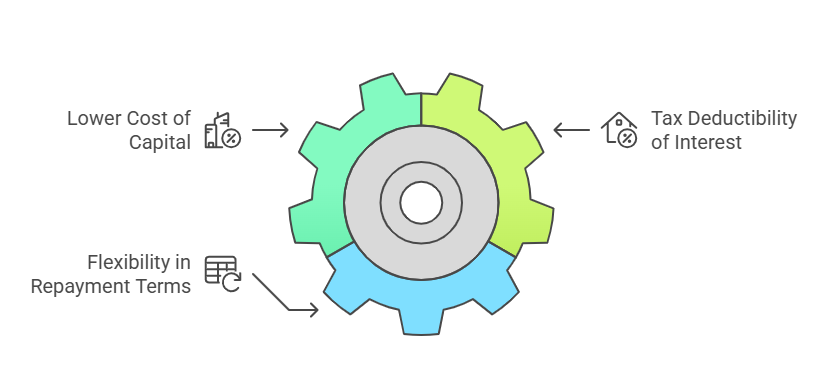

Advantages of Shareholder Loans

Lower Cost of Capital

One of the primary advantages of shareholder loans is their lower cost of capital compared to traditional bank loans. Since shareholder loans don’t require the same level of underwriting and risk assessment, shareholders who have a vested interest in the company’s success may be more willing to lend money at a lower interest rate.

Tax Deductibility of Interest

Flexibility in Repayment and Terms

After going through the advantages, let’s go through the disadvantages of the shareholders loans.

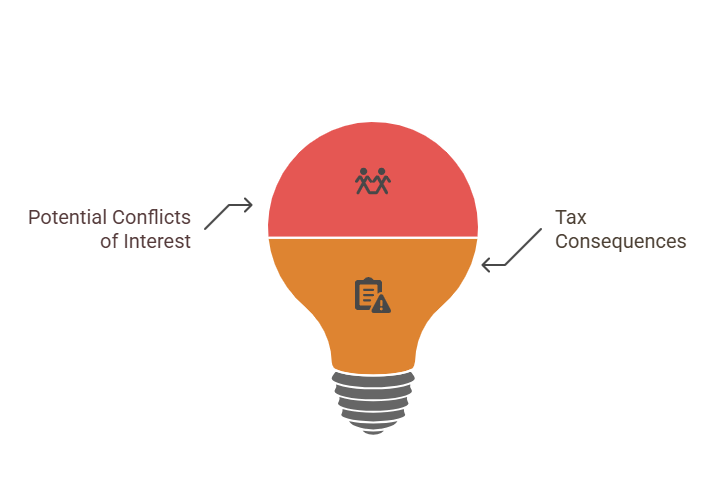

Disadvantages of Shareholder Loans

Potential Conflicts of Interest

Tax Consequences

Tax Benefits of Shareholder Loans

Tax-Deductible Interest for the Corporation

Interest Income for the Shareholder

Income Splitting Opportunities

Repayment Considerations

Repayment Timeline

Interest Payments

Here is a thread of people discussing the various nitty gritties of repaying shareholder loans.

Went through all the important considerations of shareholder loans? Let’s look at the importance of professional guidance and how it helps business.

The Importance of Professional Guidance

While shareholder loans offer flexibility and potential tax benefits, improper structuring can lead to significant tax consequences. Tax professionals can provide valuable guidance in structuring shareholder loans, ensuring compliance with regulations, and optimizing your financial position.

Partnering with One Accounting

At One Accounting, our team of dedicated Certified Public Accountants (CPAs) is committed to providing comprehensive accounting and financial services tailored to your unique needs. With expertise spanning various industries, we can help you navigate the intricacies of shareholder loans and develop strategies to achieve your financial goals.

From bookkeeping and corporate tax planning to personalized financial advisory, One Accounting is your trusted partner in managing your business finances effectively. Our focus on accuracy, efficiency, and strategic insight ensures that you have the support and guidance you need to make informed decisions and drive your business forward.

Conclusion

Shareholder loans can be a powerful financial tool for businesses and self-incorporated individuals, offering flexibility in managing cash flow and supporting growth. By understanding the purpose, advantages, disadvantages, tax implications, and repayment considerations of shareholder loans, you can make informed decisions and leverage this option effectively.

Don’t navigate the complexities of shareholder loans alone. Partner with the experienced professionals at One Accounting to unlock the full potential of your business finances. Contact us today to schedule a consultation and take the first step towards achieving your financial objectives with confidence.