Personal Real Estate Corporation (PREC)

Effective 1 October 2020, Realtors in Ontario can form a Corporation called Personal Real Estate Corporation (PREC). This allows for their self-employed revenue to be paid into a PREC. This can bring about certain tax benefits, including significant tax savings in some cases. This guide is designed to provide a high-level understanding of how PREC’s work and the related implications.

Difference Between Sole Proprietorship and Corporation:

Sole Proprietorship

All income or losses are taxed to the owner as personal income. This flow-through taxation is a significant benefit for many owners. However, a sole proprietorship also provides no liability protection for the owner. The owner is personally responsible for all liabilities, placing his or her assets at risk.

Corporation

A corporation is a legal entity that is separate from its owners, called shareholders. The shareholders do not necessarily operate the business. Instead, shareholders elect a board of directors who then elects the corporation’s officers to operate the business. Depending on the corporation, shareholders may also serve as officers.

As a separate legal entity, corporations pay taxes on profits. After taxes, profits are distributed as dividends to shareholders who then pay personal income tax on the dividends. Because they are separate legal entities, corporations provide liability protection. Incorporation is the legal process by which a business entity is formed.

What Exactly is a PREC?

A professional corporation is a corporation that provides the services of a member of a profession that is regulated by a governing professional body. Certain regulated professions are permitted to form professional corporations under their governing regulations. Realtors are regulated by the Real Estate Council of Ontario (“RECO”) and are permitted to form PRECs under TRESA.

A professional corporation allows a professional to benefit from some of the tax advantages available to traditional private corporations while protecting the public by ensuring that the professional remains professionally regulated, disciplinable, and liable for the professional services provided through the professional corporation.

Limited Liability for PREC's:

The difference between a professional corporation and a non-professional corporation is limited liability. If you incorporate your consulting business and you get sued, you will generally only lose the amount you invested. If you are not incorporated, you could potentially lose all of your assets.

If you are a PREC and are sued for malpractice, it will be a claim against your liability insurance. The corporation cannot protect you.

However, if you default on a loan, your assets are protected by the corporation.

Who can own shares in my PREC?

Only you as the “controlling individual” will be able to act as a director, officer and holder of voting shares in your PREC. However, you can issue non-voting shares in your PREC to an “affiliated person” which the Regulation defines as:

- a spouse of the controlling individual,

- a child of the controlling individual,

- a corporation, all the shares of which are beneficially owned by one or more of the controlling individual and their spouse or child, or

- a trust, all the beneficiaries of which are one or more of the controlling individual and their spouse or child.

The ability for an affiliated person to hold non-voting shares in you are the PREC allows for flexibility in terms of issuing dividends to your immediate family members or another corporation, such as a Hold Co., which may be part of the tax planning strategy that you and your accountant develop.

Tax Planning Strategy

As an unincorporated realtor, you could be subject to the highest marginal tax rate (depending on your income, can be as high as 53.53%). As a PREC, the tax rate is much lower and set at 12.5%. The additional tax savings can then be used to build your investment portfolio.

1. Tax deferral:

a. As an unincorporated realtor, you could be subject to the highest marginal tax rate (depending on your income, can be as high as 53.53%). As a PREC, the tax rate is much lower and set at 12.5%. The additional tax savings can then be used to build your investment portfolio.

2. Split your income:

a. You can pay your family members wages or issue them dividends. The catch is that, when paying wages, the wages must be for “reasonable services performed”, which means your family members must be actively engaged in the business.

b. Actively engaged is usually considered as at least 20 hours a week

3. Salary vs Dividend:

a. You have the opportunity to pay yourself either a salary or dividends. If you pay yourself a salary, you will still need to remit CPP.

b. But if you pay yourself a dividend, CPP contributions are not required, leaving you with excess cash to invest in other income-producing investments.

4. Use Marginal tax rates:

a. Canada’s marginal income tax regime means that the more money you earn in a year, the higher your tax rate will be. Lower-earning years could reduce your tax rate—which explains why it may make sense to withdraw funds during a slow year.

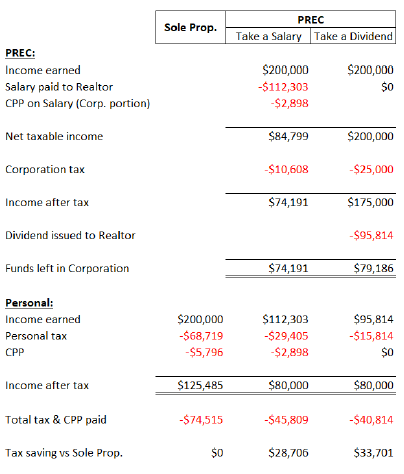

Case Study

Ms. X receives $ 200 000 in income as a Realtor during the year. Ms. X only needs $ 80 000 to maintain her lifestyle and wants to use any excess income for investing purposes. How does a PREC assist in deferring taxes?

A complex process

Tax planning around a PREC can be a complex process with multiple considerations. If you require support in navigating this new world of incorporation contact us!