GST/HST for Canadian Businesses: A Complete 2025 Guide

Managing GST/HST obligations can be challenging for Canadian businesses of all sizes. Whether you’re a startup or an established company, understanding the ins and outs of Canada’s tax system is crucial for compliance and financial accuracy.

This guide curated by experts breaks down everything you need to know about GST/HST for 2025, including recent updates and practical tips to help your business stay compliant and financially sound.

Let’s start by understanding the fundamental differences between GST and HST, which form the backbone of Canada’s consumption tax system.

Understanding GST and HST

What is GST?

The Goods and Services Tax (GST) is a federal tax of 5% applied to most goods and services sold in Canada. This nationwide tax affects virtually all Canadian businesses, forming the foundation of the indirect tax system.

What is HST?

The Harmonized Sales Tax (HST) combines the federal GST with provincial sales taxes into a single tax. This streamlined approach simplifies tax collection and remittance for businesses operating across multiple provinces.

Which provinces use HST?

As of 2025, five provinces use HST:

- Ontario: 13% (5% federal + 8% provincial)

- New Brunswick: 15% (5% federal + 10% provincial)

- Newfoundland and Labrador: 15% (5% federal + 10% provincial)

- Prince Edward Island: 15% (5% federal + 10% provincial)

- Nova Scotia: 14% (5% federal + 9% provincial) – Note the upcoming rate change effective April 1, 2025

Other provinces maintain separate GST and Provincial Sales Tax (PST) systems, requiring businesses to manage multiple tax obligations.

Now that you understand what GST/HST is, let’s examine which businesses are required to register for these taxes and when voluntary registration might make sense.

Who Needs to Register

Mandatory Registration

You must register for GST/HST when your business exceeds $30,000 in taxable revenue over four consecutive calendar quarters or in a single calendar quarter. This threshold applies to sole proprietors, partnerships, and corporations alike.

What counts toward the $30,000 threshold?

- Sales of taxable goods and services at regular rates

- Zero-rated sales (taxable at 0%)

- Services performed outside Canada that would be taxable if performed within Canada

Voluntary Registration

Even if your business hasn’t reached the $30,000 threshold, you might benefit from voluntary registration. This allows you to do the following:

- Claim Input Tax Credits (ITCs) on business purchases

- Project a more established image to clients

- Avoid retroactive tax collection if you approach the threshold

Special Cases

Different rules apply to the following:

- Public service bodies like municipalities and universities

- Charities and non-profit organizations

- Non-resident businesses selling to Canadian customers

For GST/HST Canadian businesses in these special categories, specific exemptions and obligations may apply based on your organization’s structure and activities.

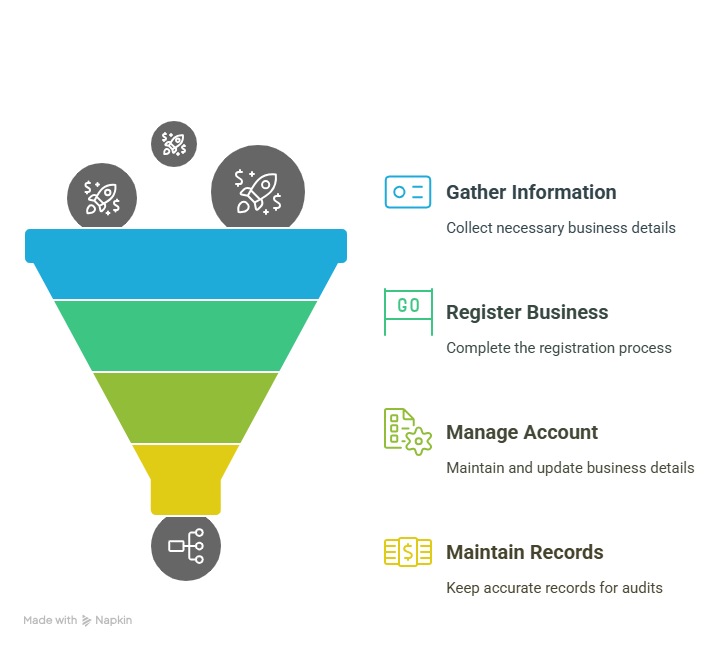

Once you’ve determined that registration is necessary or beneficial for your business, the next step is understanding how to register and manage your GST/HST account with the CRA

How to Register and Manage Your Account

You can register for GST/HST through the following:

- CRA My Business Account (online)

- Phone registration (1-800-959-5525)

- Mail or fax (Form RC1)

What You Need

Be prepared with the following:

- Your Business Number (BN)

- Legal name and business structure

- Fiscal year details

- Expected annual revenue

- Effective date of registration

Managing Your Account

Once registered, you’ll need to do the following:

- Update contact information when it changes

- Modify registration details if business structure changes

- Cancel registration if you cease operations

- Maintain accurate records for potential CRA audits

After successfully registering, your business must begin charging and collecting GST/HST on taxable supplies, which involves understanding several key concepts.

Charging and Collecting GST/HST

Place of Supply Rules

The GST/HST rate you charge depends on where the supply is made

- For goods: typically where the goods are delivered

- For services: generally where the service is performed

- For intangible property: where the property is used

These “place of supply” rules help GST/HST Canadian businesses determine which rate to charge when operating across multiple provinces.

When to Start Charging

Begin charging GST/HST on the earliest of:

- The day of your first taxable sale after registration

- The effective date of your registration

Zero-rated vs. Exempt

Understanding the difference is crucial between:

- Zero-rated supplies (taxed at 0%): Businesses can claim ITCs, includes basic groceries, agricultural products, prescription drugs

- Exempt supplies (not subject to GST/HST): Businesses cannot claim ITCs, includes healthcare services, educational services, financial services

Proper documentation is essential when charging GST/HST, which brings us to the requirements for invoicing and recordkeeping that every business must follow.

Invoicing and Recordkeeping

GST/HST-compliant Invoices

Your invoices must include the following:

- Your business name and GST/HST registration number

- Invoice date and number

- Customer name and address

- Description of goods or services

- GST/HST amount charged (or statement that tax is included)

- Terms of payment

Receipts and Ledgers

Maintain detailed records of the following:

- Sales and revenue

- Purchases and expenses

- GST/HST collected and paid

- Import/export documentation

- All tax returns and supporting documents

Keep these records for six years from the end of the tax year they relate to.

Best Practices

Consider implementing the following:

- Cloud-based accounting systems to automate tax calculations

- Digital receipt management to ensure nothing gets lost

- Regular reconciliation of GST/HST accounts

- Quarterly reviews of compliance procedures

While collecting GST/HST is one side of the equation, recovering the tax you pay on business purchases through Input Tax Credits is equally important for your bottom line.

Invoicing and Recordkeeping

What are ITCs?

Input Tax Credits allow your business to recover GST/HST paid on business-related purchases and expenses. This is a significant advantage for GST/HST Canadian businesses, effectively making these taxes a flow-through rather than a cost.

Who Can Claim?

You can claim ITCs if you have the following:

- You’re registered for GST/HST

- The expense is for business use

- You have proper documentation (invoices, receipts)

- The expense isn’t specifically disallowed

Common Mistakes to Avoid

Watch out for the following:

- Claiming personal portions of expenses

- Missing documentation for claims

- Claiming exempt supplies

- Incorrect calculation of partial ITCs

- Failing to meet timeline requirements

Once you’ve mastered collecting GST/HST and claiming ITCs, you’ll need to file returns and remit the net amount to the CRA according to a specific schedule.

Filing and Remitting GST/HST

Filing Frequencies

Your filing frequency depends on annual taxable sales:

- Monthly: over $6 million

- Quarterly: $1.5 million to $6 million

- Annual: under $1.5 million

How to File

As of 2025, electronic filing is mandatory for most businesses. Options include the following:

- CRA My Business Account

- GST/HST NETFILE

- Electronic filing through approved software

Remitting Payments

Payment due dates align with your filing frequency:

- Monthly/Quarterly: One month after the end of the reporting period

- Annual: Three months after your fiscal year-end

Payment options include online banking, pre-authorized debit, credit card, and wire transfers.

How to Correct a Return

If you discover an error in a previous return:

- For the current reporting period: adjust your next return

- For past periods: file a GST/HST adjustment form

- For substantial corrections: consider a voluntary disclosure

Speaking of electronic filing, it’s important to note that recent changes have made this method mandatory for most businesses, with significant implications for compliance.

Mandatory Electronic Filing (2024 Onward)

Who Must File Electronically

All GST/HST Canadian businesses with reporting periods starting January 1, 2024, or later must file electronically, with limited exceptions.

Exemptions

Exemptions apply only to the following:

- Registered charities

- Selected listed financial institutions (SLFIs)

- Businesses with specific technological barriers (rare)

How to Comply

Meet this requirement by doing the following:

- Setting up CRA My Business Account

- Using compatible accounting software with direct CRA filing

- Working with a tax professional who can file electronically

Penalties for Paper Filing

Non-compliance can result in the following:

- Penalties of $100 to $2,500 depending on the number of infractions

- Delays in processing returns and credits

- Potential compliance actions by the CRA

In addition to understanding these ongoing requirements, businesses must stay informed about upcoming tax rate changes, such as the significant adjustment coming to Nova Scotia in 2025.

Nova Scotia HST Rate Change (Effective April 1, 2025)

Overview of Change

Nova Scotia is decreasing its provincial portion of HST from 10% to 9%, bringing the total HST rate to 14% (5% federal + 9% provincial) effective April 1, 2025.

Key Dates and Impact

For GST/HST Canadian businesses operating in Nova Scotia following are the considerations:

- Update point-of-sale systems by April 1, 2025

- Adjust pricing and tax calculations

- Communicate changes to customers

- Apply transition rules correctly

Transition Rules

Based on CRA NOTICES 342 and 343:

- For goods: Generally, the tax rate applies based on when the customer pays or when the goods are delivered

- For services: The rate applies based on when the service is rendered

- For real property: Special rules apply to construction contracts and residential properties

How Businesses Should Prepare

Take these steps now:

- Review and update accounting software

- Train staff on the new rate and timing

- Audit invoicing templates and systems

- Plan for transitional inventory and pricing

During economic challenges or unusual circumstances, businesses should be aware that the CRA sometimes offers support measures to ease compliance burdens.

Conclusion

Navigating GST/HST requirements is a crucial responsibility for Canadian businesses. From registration and charging the correct rates to filing returns and claiming ITCs, proper GST/HST management contributes significantly to your business’s financial health and compliance standing.

With the 2025 changes in Nova Scotia and the continuing electronic filing requirements, staying updated with CRA regulations is more important than ever. Remember that GST/HST Canadian businesses that maintain proper documentation, understand their obligations, and file on time will avoid penalties and maximize their tax efficiency.

One Accounting can help simplify your GST/HST compliance with expert guidance tailored to your business needs. Our team of experienced CPAs will ensure you’re meeting all requirements while maximizing available credits and minimizing your administrative burden. Contact us today to transform your GST/HST management from a challenge into a strategic advantage for your busines