Financial Planning For Retirement Calgary: Your Complete Guide to a Secure Future

Are you prepared for your golden years in Calgary? Financial planning for retirement in Calgary requires specialized knowledge of local economic factors, Alberta tax laws, and investment opportunities unique to the region.

At One Accounting, we understand that retirement planning in Calgary comes with its own set of challenges and opportunities. Whether you’re decades away from retirement or approaching it in the next few years, developing a comprehensive strategy tailored to Calgary’s economic landscape can make all the difference between financial stress and peace of mind.

Understanding Retirement Planning in Calgary's Economic Context

- An economy historically tied to energy sector fluctuations

- Higher average housing costs compared to many Canadian cities

- Alberta’s tax advantage (no provincial sales tax)

- Calgary’s higher-than-average cost of living

- Seasonal expense variations due to extreme winter conditions

Effective financial planning for retirement in Calgary requires understanding these factors. One Accounting’s financial advisors help you navigate these regional considerations with confidence by bringing local expertise.

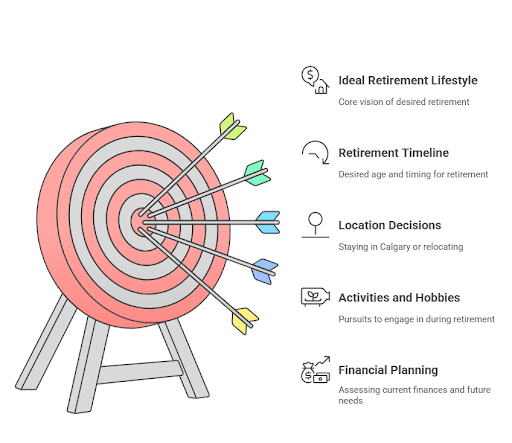

Setting Realistic Retirement Goals for Calgary Living

- When do you want to retire?

- Will you stay in Calgary or relocate during retirement?

- What activities and hobbies will you pursue?

- Do you plan to travel extensively?

- Will you downsize your home?

Assessing Your Current Financial Position

- All retirement savings accounts (RRSPs, TFSAs, pension plans)

- Other investments and assets

- Current income sources

- Existing debts and liabilities

- Monthly expenses and spending patterns

This thread explores a Calgary resident looking to assess and take control of their financial life through a certified tax planner.

Calgary’s economic environment including local housing market values, energy costs, and other region-specific expenses should factor into this assessment. You can conduct a thorough financial review with One Accounting’s help that accounts for these local factors, giving you a realistic starting point for your retirement planning journey.

Investment Strategies Tailored to Calgary's Economic Landscape

- Diversification beyond energy stocks, despite their prominence in local investment portfolios

- Real estate investments that leverage Calgary’s growing neighborhoods

- Dividend-generating investments for steady retirement income

- Balanced exposure to different economic sectors to protect against local economic downturns

- Tax-efficient investment vehicles that maximize Alberta’s tax advantages

Navigating Alberta's Tax Landscape in Retirement

- Strategic RRSP withdrawals to minimize lifetime tax burden

- Optimal use of TFSA contribution room

- Income splitting with your spouse to reduce overall tax liability

- Timing of CPP and OAS benefits to maximize after-tax income

- Tax-efficient drawdown strategies from various retirement accounts

Maximizing Government Benefits for Calgary Retirees

- When to start collecting CPP (as early as 60 or as late as 70)

- OAS clawback thresholds and how to minimize them

- Guaranteed Income Supplement eligibility for lower-income retirees

- Alberta Seniors Benefit and other provincial programs

- Tax implications of government benefits

Healthcare Planning for Calgary Retirees

- Prescription medications not covered by Alberta’s seniors’ drug program

- Dental care and vision expenses

- Home care services or long-term care

- Medical equipment and mobility aids

- Supplemental health insurance premiums

These healthcare considerations often get overlooked in retirement planning but can significantly impact your financial security. One Accounting can help you estimate potential healthcare costs and incorporate them into your comprehensive retirement plan.

Estate Planning Within Alberta's Legal Framework

- A valid will that reflects your current wishes

- Power of attorney for financial and health decisions

- Personal directives (living will)

- Beneficiary designations on registered accounts and insurance policies

- Tax-efficient transfer strategies for your estate

Now that you’ve got estate planning covered, let’s see why engaging a Calgary-based financial planner can be a game-changer in your retirement planning journey.

Engaging a Calgary-Based Financial Planner

When selecting a financial planner for retirement planning in Calgary, look for the following criteria:

- Relevant certifications and qualifications

- Experience working with clients in similar situations

- Knowledge of Alberta’s tax laws and financial environment

- A comprehensive approach that addresses all aspects of retirement planning

- Clear communication and regular review processes

Financial advisors bring specialized knowledge of Calgary’s economic landscape to your retirement planning process. Our advisors combine technical expertise with local insights to create strategies that work specifically for Calgary residents.

Real-World Example: Financial Planning for Retirement in Calgary

- Optimizing their investment portfolio to balance growth and protection

- Implementing tax-efficient withdrawal strategies from their RRSPs and TFSAs

- Timing their CPP and OAS benefits to maximize lifetime income

- Creating an estate plan that minimized tax implications for their beneficiaries

- Establishing a healthcare fund for expenses not covered by Alberta Health

Conclusion: Taking Action on Your Retirement Planning

Don’t leave your retirement security to chance. One Accounting’s team of financial advisors specializes in helping Calgary residents navigate the complexities of retirement planning with confidence. Our comprehensive approach ensures all aspects of your financial future are addressed, from tax optimization to estate planning.

Contact One Accounting today to begin your personalized financial planning for retirement in Calgary. Our expert advisors are ready to help you transform retirement uncertainty into clarity and confidence.