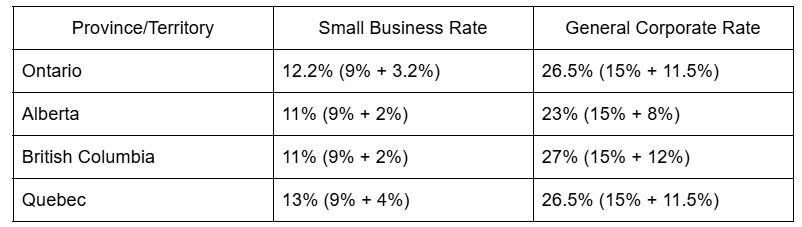

In addition to the federal corporate tax, every province and territory in Canada imposes its own corporate tax rate. These rates vary depending on your location and whether your business qualifies for the Small Business Deduction.

Here’s a breakdown of combined Canada corporate tax rates in 2025:

These rates can significantly impact your bottom line, especially for growing businesses earning well over the $500,000 small business threshold.

If your business operates in multiple provinces, or you’re planning to expand, understanding these regional variations can help you choose where to incorporate or how to structure your operations.

Now that you’ve seen how both levels of government tax your business, let’s explore how small companies can benefit the most through deductions.

Every year, businesses lose money. Not from overspending, but from simple tax filing mistakes. Here are a few you should keep an eye out for:

- Missing filing deadlines: Late returns result in penalties and interest.

- Mixing business and personal expenses: This muddies your records and triggers CRA scrutiny.

- Overestimating your eligibility for the SBD: This is especially common for associated companies or firms with significant investment income.

- Poor record-keeping: Lost receipts mean lost deductions.

- Not reviewing your tax position quarterly: Waiting until year-end to assess your tax obligations is too late.

Avoiding these mistakes can protect your profits and your peace of mind. And if you’re not sure where you stand, it might be time to call a pro.