These platforms categorize expenses automatically, track sales tax, generate financial reports, and often integrate with other business tools you’re already using.

However, these do have their limitations. Here is a Reddit user discussing the shortcomings and wondering if a specialized bookkeeping service in Toronto is the solution.

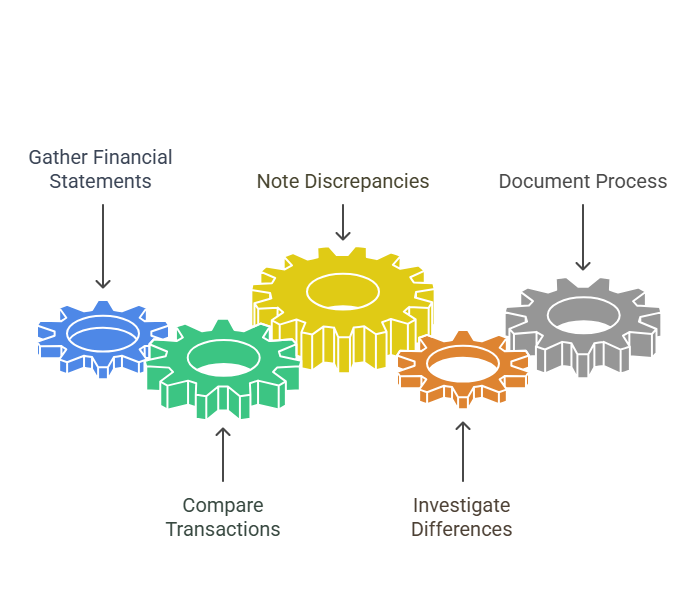

Account reconciliation is among the most valuable bookkeeping tips for Toronto entrepreneurs. This process involves comparing your internal financial records against external statements (like bank and credit card statements) to ensure everything matches up.

Here’s how to effectively reconcile your accounts as listed below:

- Gather all financial statements for the period

- Compare each transaction in your books against the statements

- Note any discrepancies or unexplained items

- Investigate and resolve differences

- Document the reconciliation process for future reference

By reconciling monthly, you catch errors early and prevent small issues from snowballing into major accounting problems. It also helps identify potential fraud or unauthorized transactions before they cause significant damage.

Now that your books are accurate and up-to-date, let’s tackle one of the most important aspects of bookkeeping for Toronto businesses: tax compliance.