Bank of Canada Cuts Benchmark Interest Rate by 25 bps as Trump Escalates Tariffs

The Bank of Canada’s interest rate has been reduced by 25 basis points, bringing the overnight rate to 2.75%. This decision comes as Canada faces increasing economic uncertainty due to growing trade tensions with the United States. It’s important to understand the factors behind the Bank of Canada’s recent decision from an expert’s view.

While the Canadian economy started 2025 in a strong position with inflation near the 2% target, recent developments have prompted the central bank to support economic stability.

Why Did the Bank of Canada Cut Interest Rates?

The Bank of Canada interest rate reduction reflects the central bank’s concern about how U.S. tariffs and trade conflicts might affect Canadian economic growth.

Trade Tensions with the United States

The Bank of Canada noted that while previous interest rate cuts have boosted economic activity, particularly in consumption and housing, the economy will likely slow in the first quarter of 2025 as trade conflicts intensify.

Current Economic Indicators

- Inflation remains close to the 2% target (currently at 1.9%)

- Employment growth had strengthened from November through January

- The unemployment rate declined to 6.6%

- Job growth stalled in February

- Wage growth has shown signs of moderation

The temporary suspension of the GST/HST had lowered some consumer prices, but inflation is expected to increase to about 2.5% in March when this tax break ends.

How Will This Rate Cut Affect Canadians?

The latest Bank of Canada interest rate reduction will have several impacts on everyday Canadians and the broader economy.

Benefits for Borrowers

Lower interest rates typically make borrowing less expensive, which can benefit:

- Homeowners with variable-rate mortgages

- Individuals with lines of credit or variable-rate loans

- Businesses looking to invest or expand

Mortgage holders may see their monthly payments decrease, providing some financial relief. New homebuyers might find borrowing costs more affordable, potentially stimulating the housing market further.

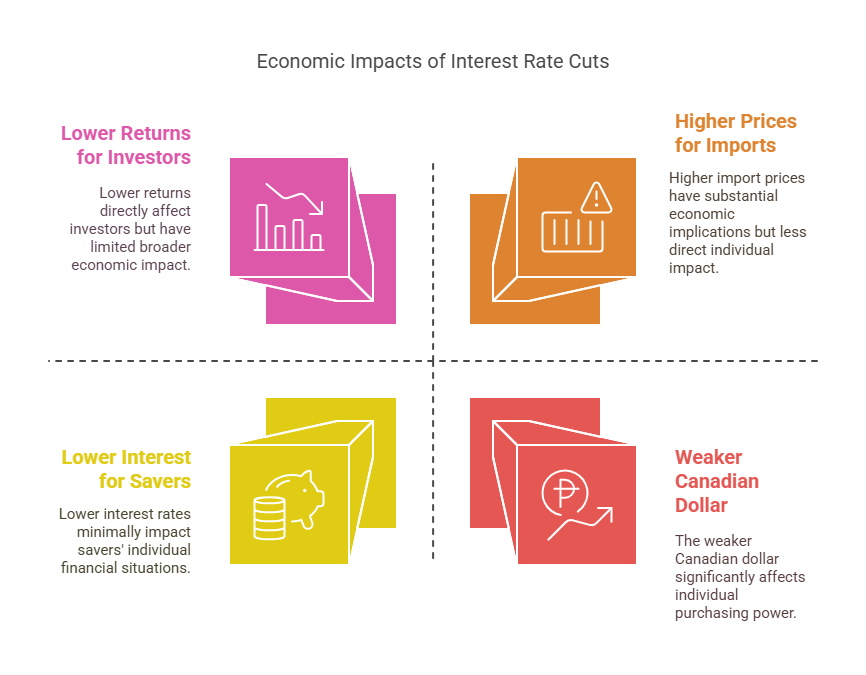

Potential Challenges

- Savers will earn less interest on their deposits

- Fixed-income investors might see lower returns

- The Canadian dollar could weaken against other currencies

- Higher prices for imported goods due to a weaker dollar

Watch this video to learn more about the Bank of Canada’s decision to cut interest rates by 25 basis points, bringing the benchmark rate down to 2.75%.

Economic Outlook Following the Interest Rate Decision

The Bank of Canada’s interest rate reduction comes at a time of significant economic uncertainty. The Governing Council will be carefully assessing both the downward pressures on inflation from a potentially weaker economy and the upward pressures from higher costs due to tariffs.

Growth Forecasts

- Slower economic growth in the first quarter of 2025

- Continued pressure on businesses due to trade uncertainties

- A potential disruption to the recovery in the job market

The surge in exports ahead of tariff implementation has partially offset the negative impact of slowing domestic demand, but this effect is likely temporary.

Inflation Expectations

The central bank has emphasized that it will closely monitor inflation expectations while maintaining its commitment to price stability. The Bank of Canada’s interest rate decisions will continue to be guided by these observations.

What to Expect in the Coming Months

Factors That Will Influence Future Rate Decisions

- The actual impact of U.S. tariffs on Canadian businesses

- Changes in consumer spending and business investment

- Inflation data following the end of the GST/HST tax break

- Employment figures in March and April

- Global economic conditions, particularly in the U.S. and China

Conclusion

As we move forward, both consumers and businesses should carefully monitor economic developments and prepare for potential volatility. The next Bank of Canada announcement in April will provide further insights into how the central bank views the evolving economic landscape.

Want to see how One Accounting can help you navigate the financial implications of changing interest rates? Get started today with a solution that grows alongside your business.