Navigating the Complexities of EIFEL: A Comprehensive Guide

Are you a business owner or financial professional looking to understand the recently introduced Excessive Interest and Financing Expenses Limitation (EIFEL) rules? With the implementation of these new regulations, it’s crucial to grasp their implications and ensure your organization is compliant.

In this comprehensive guide, we’ll walk you through everything you need to know about EIFEL and how One Accounting can help you navigate these complexities with ease.

What are EIFEL Rules and Why Were They Introduced?

EIFEL rules were developed to address base erosion and profit shifting (BEPS) concerns, which have been a growing issue in the international tax landscape.

BEPS arises when multinational enterprises exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations, effectively reducing their overall tax liability. This practice has led to a significant loss of tax revenue for many countries, including Canada.

- Maintain the integrity of its tax base

- Discourage aggressive tax planning strategies

- Foster a level playing field for businesses operating in Canada

- Promote greater transparency and accountability in corporate tax reporting

Who Do EIFEL Rules Apply To?

The EIFEL rules apply to a broad range of entities, including corporations and trusts that have interest and financing expenses (IFE) or interest and financing revenues (IFR).

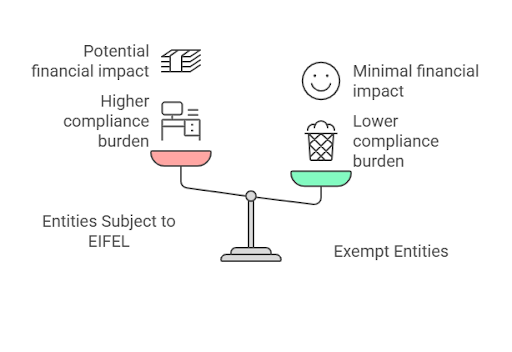

However, there are some notable exceptions. The following entities are generally excluded from the application of EIFEL rules:

- Canadian-controlled private corporations (CCPCs) with taxable capital employed in Canada below $50 million: This exemption aims to provide relief for smaller businesses that may not have the same resources or tax planning opportunities as larger corporations.

- Groups with aggregate net interest expense of $1 million or less: This de minimis threshold ensures that organizations with relatively low borrowing costs are not burdened by the additional compliance requirements imposed by EIFEL rules.

- Standalone Canadian-resident corporations and trusts with limited foreign affiliations: Entities that operate primarily within Canada and have limited exposure to international tax planning strategies may be exempt from EIFEL rules.

Understanding the affected entities is crucial, but what about the specific provisions and limitations you need to be aware of?

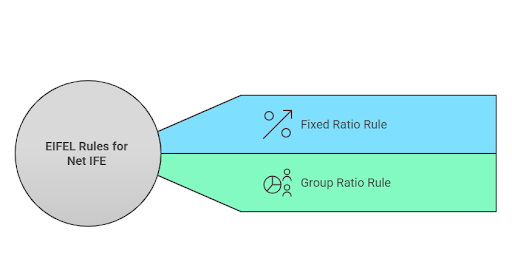

Key Provisions and Limitations

1. Fixed ratio rule:

- For taxation years beginning after September 30, 2023, and before January 1, 2024, the cap is set at 40% of adjusted taxable income (ATI).

- For taxation years beginning after December 31, 2023, the cap is reduced to 30% of ATI.

ATI is a measure of your organization’s profitability, with certain adjustments made to reflect the impact of interest and financing expenses. By limiting the deductibility of net IFE to a fixed percentage of ATI, EIFEL rules aim to ensure that excessive debt financing does not erode the tax base.

2. Group ratio rule:

- As an alternative to the fixed ratio rule, organizations may elect to apply the group ratio rule.

- Under this approach, the cap on net IFE is based on an allocated group ratio amount, which is determined using audited consolidated financial statements.

- The group ratio rule may be advantageous for organizations that are part of a multinational group and have a higher proportion of interest and financing expenses relative to their ATI.

Exceptions, Exemptions, and Reporting Requirements

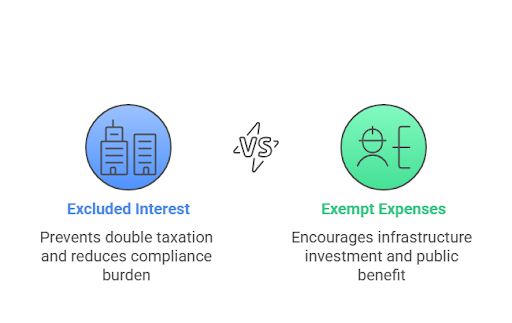

While EIFEL rules cast a wide net, there are certain exceptions and exemptions that may apply to your organization. These include the following:

- Excluded interest: If your organization has interest expenses arising from intra-group transactions with eligible Canadian corporations, you may be able to exclude these amounts from your IFE and IFR calculations. This exemption aims to prevent double taxation and reduce the compliance burden for related-party transactions.

- Exempt interest and financing expenses: Certain expenses, such as those related to Canadian public-private partnership infrastructure projects, may be exempt from EIFEL rules. This exemption recognizes the public benefit of these projects and aims to encourage investment in infrastructure development.

It’s crucial to maintain accurate records and support the deductibility of your interest and financing expenses. Failure to comply with EIFEL rules and reporting requirements may result in penalties and increased scrutiny from tax authorities.

It’s crucial to stay on top of these requirements to avoid any potential pitfalls. And how do you do that?

Navigating EIFEL with One Accounting

As businesses grapple with the complexities of EIFEL rules, seeking the guidance of experienced professionals can be invaluable.

At One Accounting, our team of dedicated Certified Public Accountants (CPAs) is well-versed in the intricacies of these new regulations and stands ready to support your organization in navigating the challenges and opportunities they present.

Our comprehensive approach to EIFEL compliance includes:

1. Assessment and Planning:

- We’ll work closely with you to assess your organization’s exposure to EIFEL rules and identify potential areas of risk or opportunity.

- Our team will develop a tailored strategy to optimize your financial structure, minimize your tax liability, and ensure full compliance with EIFEL requirements.

2. Implementation and Reporting:

- One Accounting will guide you through the process of implementing any necessary changes to your financial processes and systems to align with EIFEL rules.

- We’ll ensure that your organization is accurately tracking and reporting its interest and financing expenses and revenues, and that all required documentation is maintained.

- Our team will prepare and file Schedule 130 on your behalf, ensuring timely and accurate reporting to tax authorities.

- As EIFEL rules and related regulations evolve, One Accounting will keep you informed of any changes that may impact your organization.

- We’ll provide ongoing support and guidance to help you adapt to new requirements, optimize your tax position, and maintain compliance over time.

- Our team will continuously monitor your organization’s financial performance and provide proactive recommendations to maximize the efficiency and effectiveness of your tax strategy.

With our deep expertise, commitment to client success, and proactive approach, you can trust us to be your partner in navigating the complexities of EIFEL rules and achieving your financial objectives.

Contact One Accounting today to schedule a consultation and take the first step towards securing your organization’s financial future. Together, we’ll develop a roadmap for success and provide you with the peace of mind that comes from knowing your business is in expert hands.