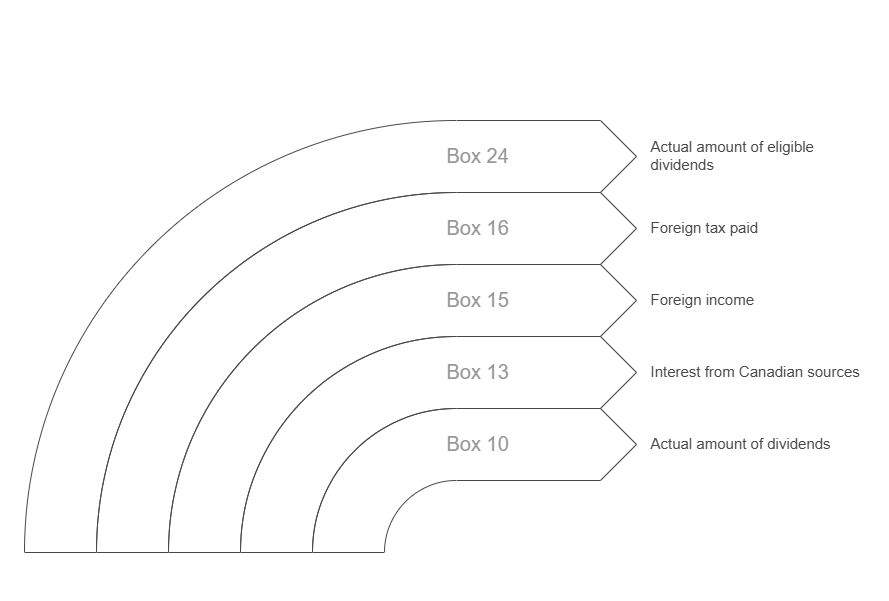

Components of a T5 Slip

A T5 slip is divided into several boxes, each representing a specific type of investment income. Understanding these boxes is key to accurately reporting your income. Some of the most important boxes include:

- Box 10: Actual amount of dividends – This box shows the total amount of dividends you received from Canadian corporations.

- Box 13: Interest from Canadian sources – Here, you’ll find the total interest income you earned from Canadian investments, such as savings accounts, GICs, and bonds.

- Box 15: Foreign income – If you received investment income from foreign sources, report it in this box.

- Box 16: Foreign tax paid – This box displays any foreign taxes you paid on your investment income, which may be eligible for a foreign tax credit.

- Box 24: Actual amount of eligible dividends – Report eligible dividends, which are taxed at a lower rate, in this box.

- Box 25: Taxable amount of eligible dividends – This box shows the taxable portion of your eligible dividends.

- Box 26: Dividend tax credit for eligible dividends – Report the dividend tax credit, which reduces your tax liability, here.

Now that you’re familiar with the key components of a T5 slip, let’s discuss how to properly report this information on your tax return.

How to Report T5 Income on Your Tax Return

When it’s time to file your taxes, you’ll need to include the information from your T5 slip on your T1 General Tax Return. Each type of investment income has a designated line where it should be reported.

For example, report interest income on line 12100, and report dividends from Canadian corporations on line 12000. Eligible dividends have their own line, 12000, and report the dividend tax credit on line 40425.

It’s crucial to report all investment income, even if you don’t receive a T5 slip for amounts under $50. Failure to do so may result in penalties and interest charges.

Let’s look at this Reddit thread that discusses the penalties incurred when T5 slip is not filed.